Higher returns and higher risks in new and improved credit scoring: BRDGE update

BRDGE exists to serve both SMEs and investors and we’ve always stayed true to the cause. After months of studying trends, speaking with business owners to understand their pain points, and evaluating the demands of our investors, we are pleased to announce a new credit scoring system that covers a broader spectrum of risks with higher returns.

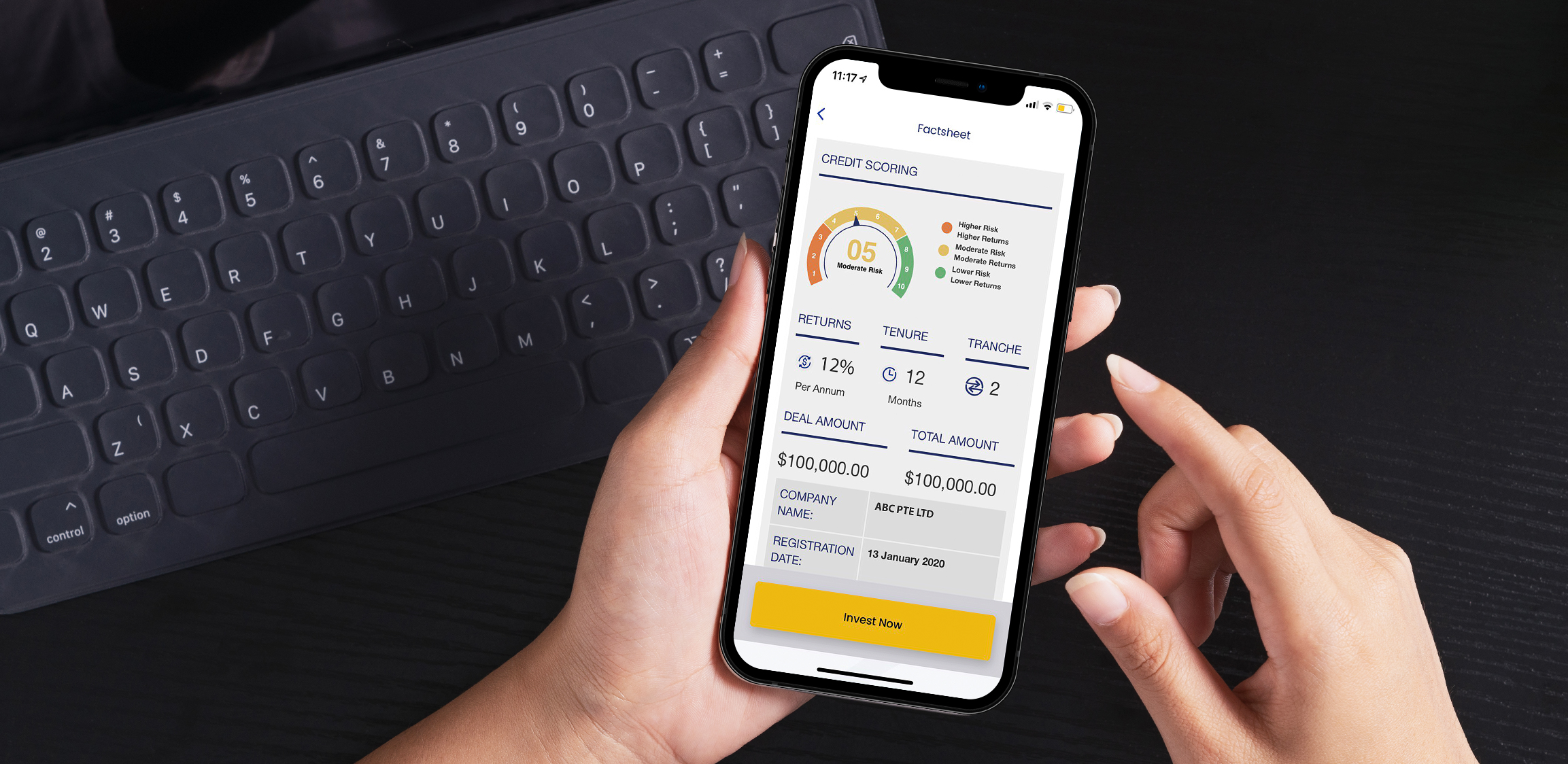

As of today, BRDGE’s credit score system will reflect SME borrowers within a range of 1-10. With this broader spectrum of credit scoring, investors can further diversify their portfolio and make more informed decisions based on their risk appetite.

The table below is the updated interest rates for BRDGE’s investments.

| Higher Risk | Moderate Risk | Lower Risk | |

| Credit Score | 1-3 | 4-7 | 8-10 |

| Interest Rate | 16% to 22% | 10% to 15% | 3% to 6% |

What does this mean for both investors and SMEs?

BRDGE is broadening its range of classification of SME borrowers on our platform so as to offer our investors a wider range of risks and rewards. Investors can now choose from a span of investment portfolios that better suit their risk appetite where higher-risk investments will yield higher returns than the other risk asset classes.

Before you decide to invest in your preferred SMEs, our credit score system allows you to calculate your risks and derive your own judgement after analysing the factsheet and conducting your own checks.

For SMEs, this new and improved credit scoring system allows investors to better understand your growth potential, even though there may be some traditional boxes that your business does not tick.

So why are these SMEs flagged as high risk, you ask?

Key insights into our credit scorecard

Our credit scoring system is proprietary to BRDGE and is built on an automated system that determines the credit scorecard of an SME after all the required data has been entered into the system. In order for BRDGE to input the data, the SME is required to provide BRDGE with extensive documentation, which include but is not limited to:

1. Company Profile (litigation profile, existing charges, company establishment, shareholders, etc)

2. Bank Statements (lowest and highest bank statements over the last 6 months)

3. Financial Statements (last 6 months)

4. Credit History (last 6 months)

5. Gurantors

6. Receivables

BRDGE credit assessment team adds on key notes such as the strengths and weaknesses of the company, purpose of loan, and any other insights that will help generate a summary of the SME.

Once the scorecard is generated ranging from numbers 1-10, investors now have an overview of the credit status of the SME before deciding whether to drill further into the factsheet of the company.

What distinguishes a lower risk SME from a higher risk SME? That all boils down to the fundamentals of the company. An SME that has a positive outlook typically ticks all the boxes in the checklist above in their documentation provided to BRDGE. However, a higher risk SME might not be able to provide all the necessary documentation or may not have as strong a foundation such as long operational period and thus are flagged as higher risk. Nevertheless, this doesn’t deem them as entirely unprofitable as they may have a strong product to go to market or a business plan that has great growth potential.

BRDGE is MAS-licensed and regulated and this means that we have risk mitigation measures in place and we conduct stringent due diligence checks on SMEs’ financial health and repayment ability to protect investors’ interest. Additionally, BRDGE credit assessment and customer service teams are in constant communication with all our SME borrowers and strive to ensure that communication remains fluid with all parties involved.

A more inclusive and fair environment for SMEs to operate and thrive

The reality is that it is harder for SMEs to access funds.

Many banks prefer to allocate their resources to large enterprises rather than to SMEs. The reason is that large enterprises have a lower risk of default and their financial statements are clear. However, SMEs are riskier mainly from the point of view of investors as they may lack clear accounting information, amongst other reasons. You may read more about that here in Pros and Cons of Debt-Based Crowdfunding in Singapore: A Guide for SMEs and Investors.

But SMEs still account for a large portion of our economy and they may just be the next big Apple if they are only given the chance.

The team at BRDGE hopes that with this step forward, our SME business owners receive the funds they need to grow and our community of investors will continue to support this spurring new businesses and enjoy higher returns.

Download the BRDGE app and join our community today: iOS App / Android App

Get the guide now!

Get the guide now!